🔥 Energy Surge Meets Memory Revival. Who Leads Next?

🔎 Weekly Market Highlights March 21, 2026

To read our full disclaimer, click here.

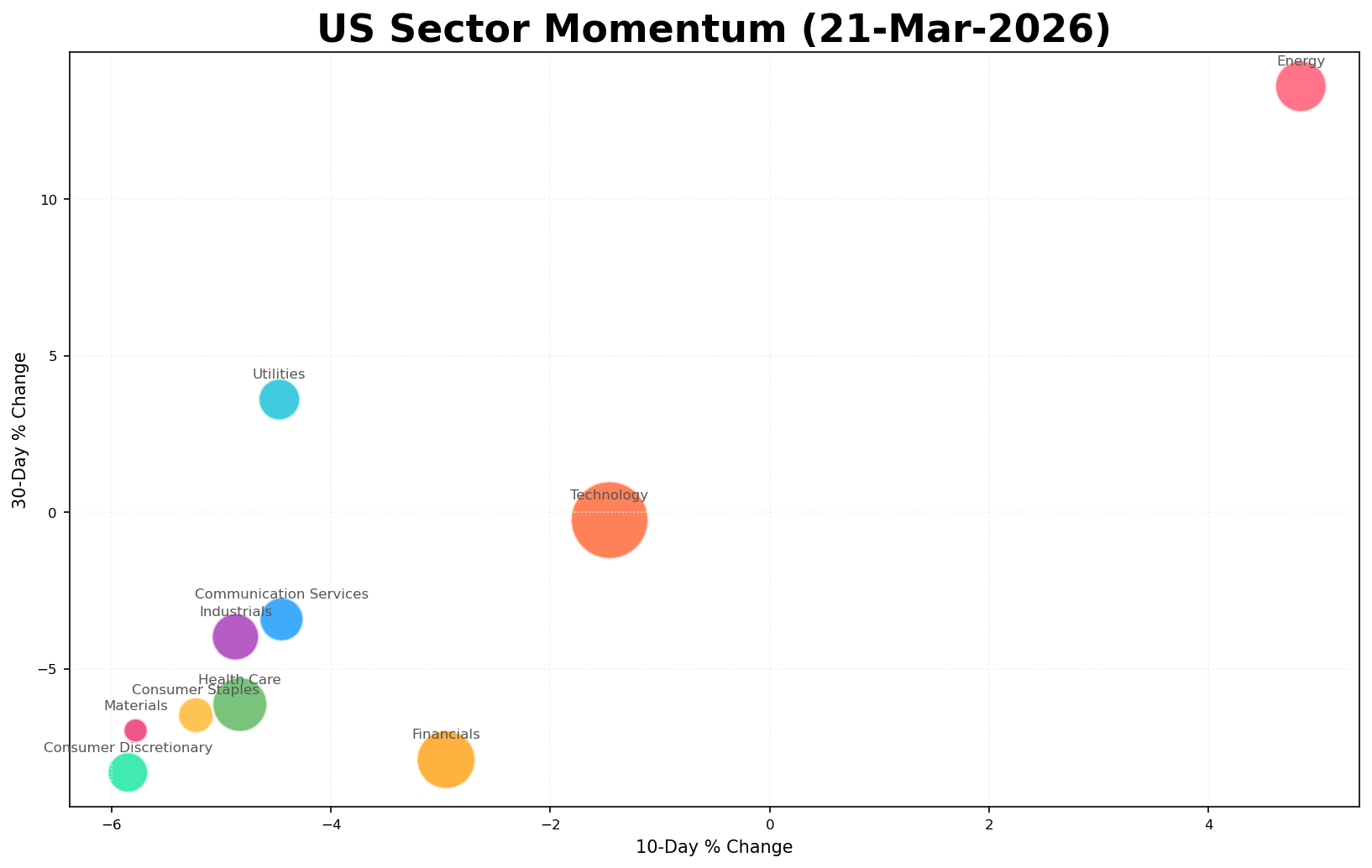

The week's dominant theme was a risk-on rotation into Energy and Value cyclicals, propelled by geopolitical risk premium re-pricing in crude. U.S.-Iran tensions escalated with strikes near Hormuz-adjacent infrastructure, driving Brent +6.7% in a single session and lifting Energy names to 52-week highs across the board.

Simultaneously, Materials saw a sharp mean-reversion bid, with nitrogen fertilizer names surging on supply-chain disruptions. Technology and Consumer Discretionary showed mixed cross-asset correlation: mega-cap AI names stabilized after oversold conditions, while legacy semiconductor equipment and memory hardware staged tentative recoveries off multi-week lows.

Defensive rotation was notably absent. Utilities and Staples underperformed, confirming that market participants are positioned risk-on into geopolitical uncertainty rather than hedging away from it.

🚨 The crowd is watching energy, this mover is hiding in plain sight.

The market’s biggest gain this week didn’t come from crude plays or AI darlings. It came from an overlooked corner of industrial infrastructure — an asset-heavy, “boring” sector that just posted its best 20-day run in years.

A structural supply-demand imbalance — not momentum — is driving institutions to quietly accumulate this theme

The real winners are currently invisible to the average investor

🎁 Paid Subscriber Additional Bonus:

Alpha Allocation & Ultra Defensive Growth Portfolio: Full access to our +26% CAGR, 22% MDD portfolios and allocation updates

Alpha Allocation Portfolio Investment Journal (2025): Explaining the rationale of every investment decision in 2025 to help you learn from us

⭐ Bonus Portfolio: Super Easy Beating Market: An easy rotation strategy that beats the market, can be done 100% on your own

⬇️⬇️⬇️

⛽ Energy — Geopolitical Risk Premium & Supply Shock

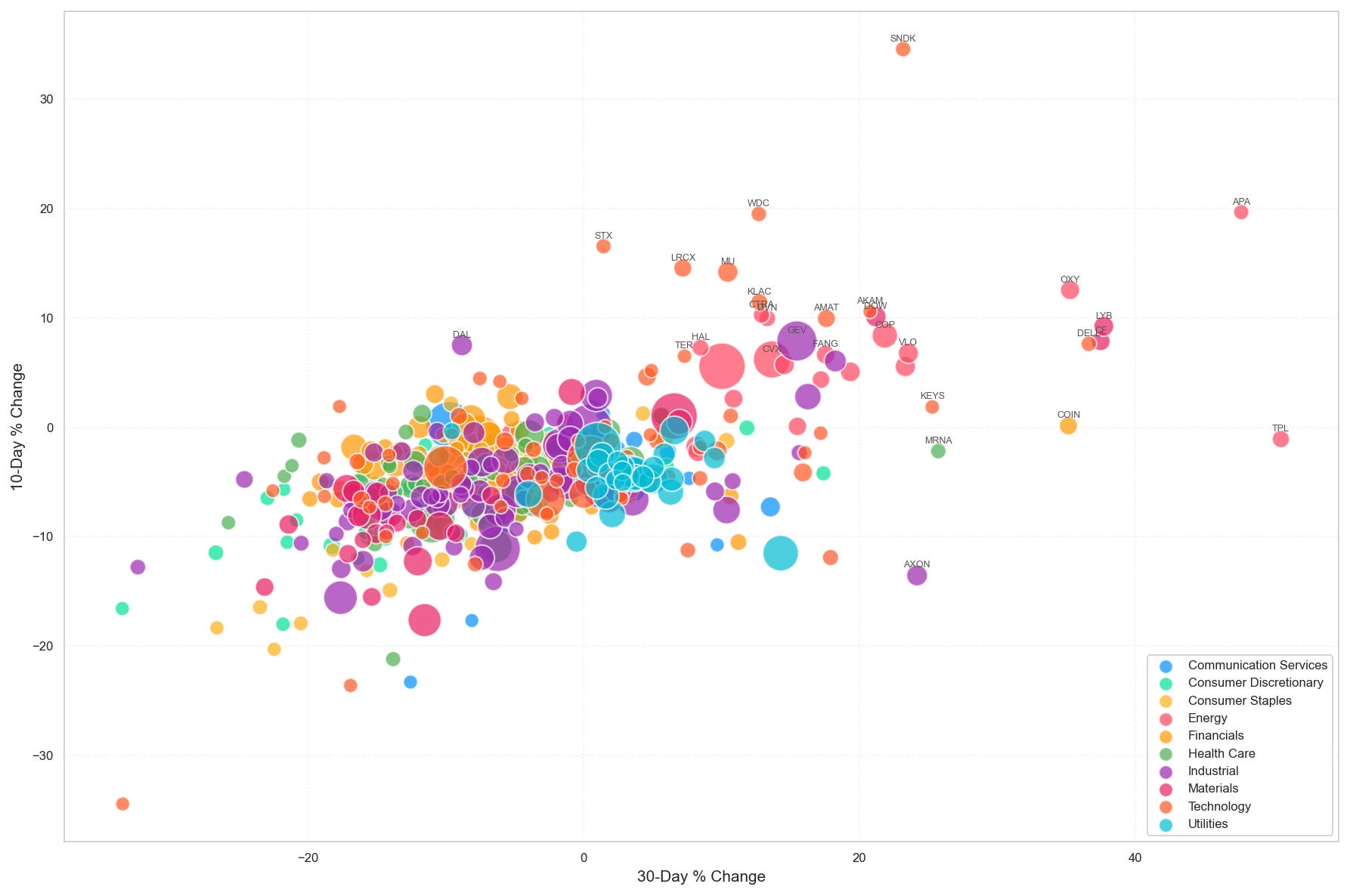

The U.S.-Iran conflict, including strikes near Middle Eastern energy infrastructure and Strait of Hormuz disruption fears, catalyzed a broad repricing of global energy assets. Brent crude surged 6.7% in a single session, with European gas spiking nearly 40% as LNG supply was disrupted. This has created a self-reinforcing bid across upstream E&P names, with multiple tickers hitting 52-week highs in the same week.

Stocks: APA (APA Corporation), COP (ConocoPhillips), OXY (Occidental Petroleum Corporation), DVN (Devon Energy Corporation), XOM (Exxon Mobil Corporation), CVX (Chevron Corporation)

Geopolitical risk premium: U.S. and Israeli strikes on Iran raised sustained Hormuz closure fears, historically the most significant supply shock scenario for global crude

Cross-sector energy lift: Energy ETFs (XLE, XOP, VDE) reached 52-week highs, confirming institutional rotation — not just retail speculation — into the theme

Supply destruction catalyst: LNG facility shutdowns added a secondary gas-price shock vector, broadening the energy bid beyond crude into integrated majors

Outlook: 4/5 — Geopolitical supply shock with medium-term runway if Hormuz risk persists

Momentum: 4/5 — APA accelerating in recent 7 days (+16.4%), broad-based lift with no deceleration

🏭 Chemicals & Fertilizers — Supply Disruption & Nitrogen Supercycle

CF Industries was the standout performer in Materials, with a structural nitrogen fertilizer supply imbalance amplifying the energy-cost tailwind. Higher natural gas prices (a key ammonia feedstock input) typically compress European nitrogen supply, redirecting pricing power to North American producers like CF Industries. LyondellBasell and Dow benefited from a broader chemicals re-rating as energy input costs and supply-demand fundamentals converged.

Stocks: CF (CF Industries Holdings, Inc.), LYB (LyondellBasell Industries N.V.), DOW (Dow Inc.)

Nitrogen supply squeeze: European gas prices spiking ~40% directly compress European ammonia/fertilizer production, shifting global pricing power to North American producers

Energy-to-chemicals pass-through: Higher crude and gas prices boost feedstock-advantaged U.S. chemical producers via margin expansion and competitive displacement of European supply

Agricultural demand baseline: Persistent global food security concerns maintain floor demand for nitrogen fertilizers regardless of short-term price cycles

Outlook: 3/5 — Moderate catalyst duration; depends on sustained European gas disruption

Momentum: 2/5 — CF fading sharply in recent 7 days (-8.2%), off 8.2% from recent peak; distribution signals present

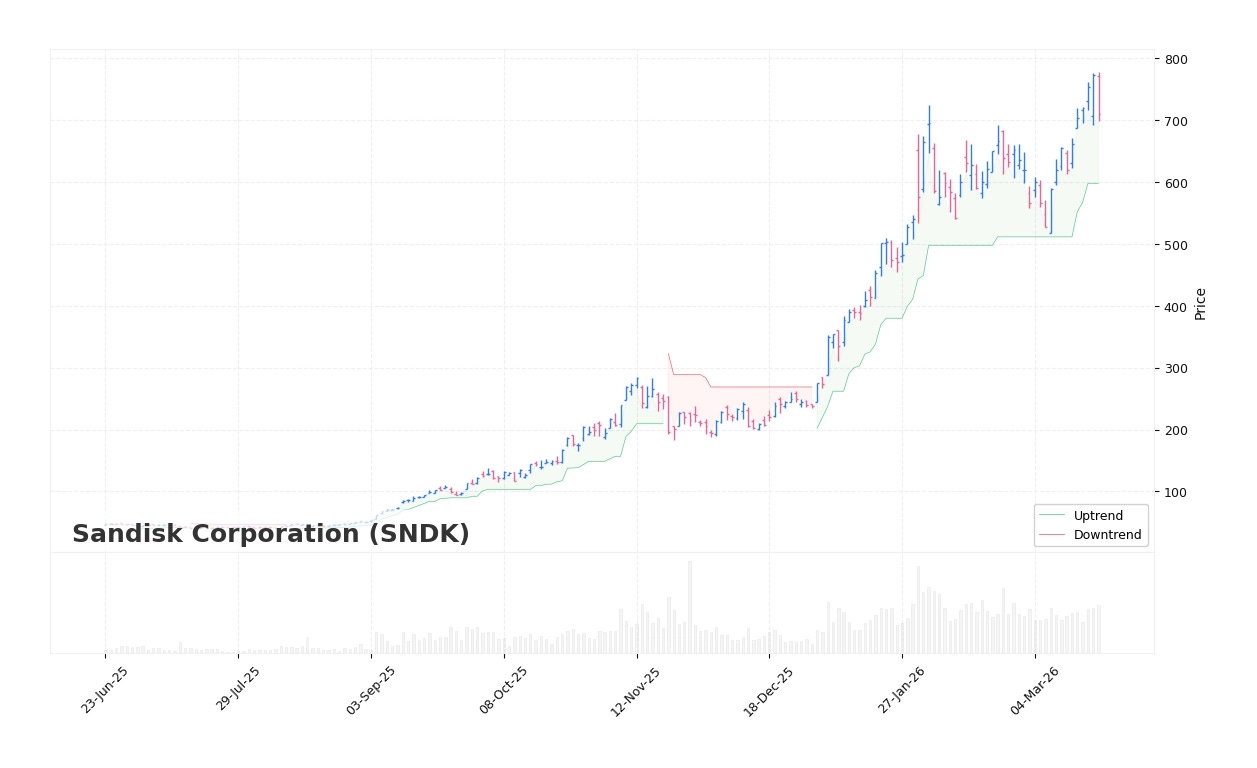

🖥️ AI Infrastructure — Downstream Hardware (Storage & Memory Recovery)

Memory and storage hardware staged a recovery off multi-month lows, with SNDK and WDC among the sharpest recent 7-day movers. This reflects a structural narrative: DRAM and NAND markets are tightening again as AI workloads expand memory content requirements, and HBM pricing is entering an upcycle. Samsung and SK Hynix reportedly raised HBM3E prices by ~20% for 2026 deliveries, confirming industry-wide repricing power.

Stocks: SNDK (Sandisk Corporation), WDC (Western Digital Corporation), MU (Micron Technology, Inc.), STX (Seagate Technology Holdings plc)

HBM upcycle confirmation: Samsung and SK Hynix raised H3E pricing by 20% for 2026 deliveries, signaling disciplined supply management and accelerating AI demand pull

NAND/DRAM tightening: After a deep oversupply-driven downturn, memory markets are returning to structural tightness driven by AI accelerator memory content growth

Data center capex expansion: Hyperscaler spending plans for 2026 include expanded memory bandwidth requirements, directly benefiting HBM and enterprise SSD suppliers

Outlook: 5/5 — Structural HBM supercycle with AI-driven multi-year demand runway

Momentum: 2/5 — SNDK and WDC surged mid-period but pulled back sharply in recent 2 sessions; off peak by -8.1% and -7.5% respectively; early distribution detected

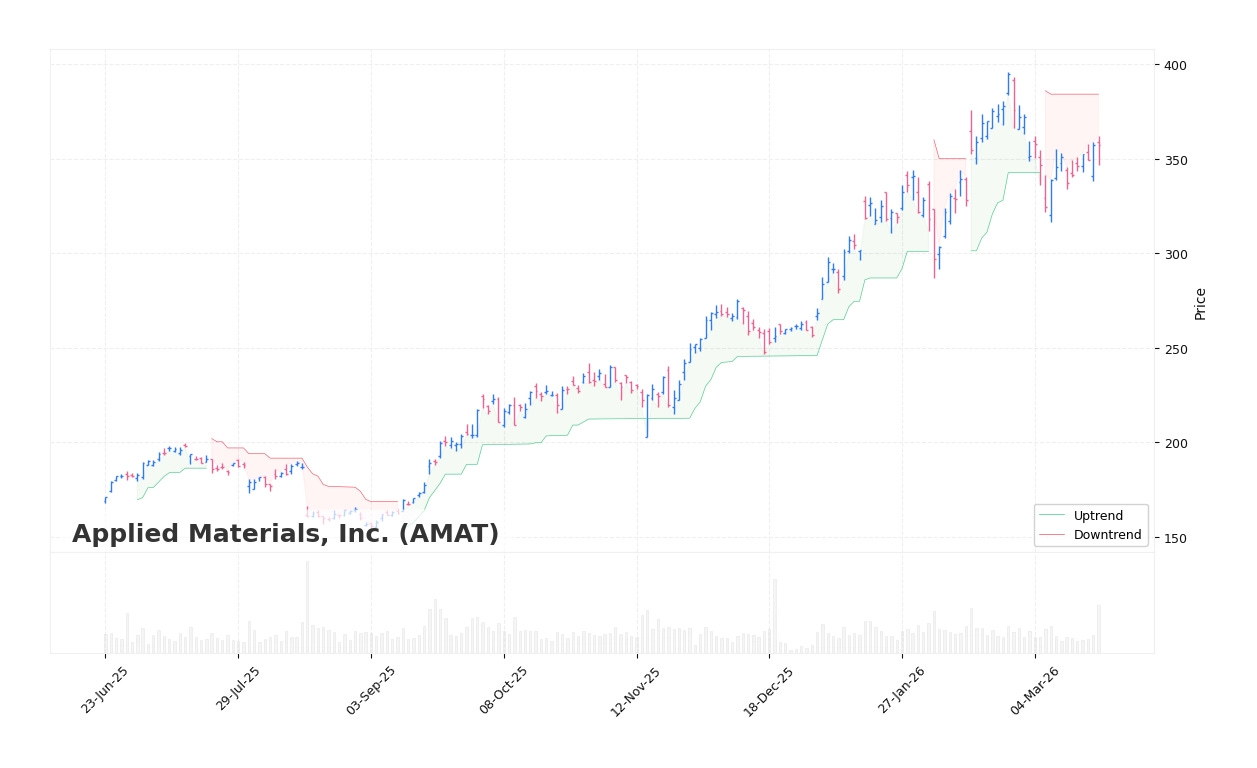

🔬 Semiconductor Equipment — Capex Recovery Laggard

Lam Research, AMAT, and KLAC all bottomed over the 20-day window and have been recovering, driven by expectations of a memory capex recovery cycle. Equipment spending typically lags memory pricing by 1-2 quarters, suggesting this group has further re-rating potential as HBM expansion investments accelerate through 2026.

Stocks: LRCX (Lam Research Corporation), AMAT (Applied Materials, Inc.), KLAC (KLA Corporation)

Memory capex cycle upturn: As DRAM/NAND producers return to profitability and HBM capacity additions accelerate, semiconductor equipment spending enters a new investment cycle

WFE spending visibility: Global semiconductor sales expected to grow 26.3% in 2026 per WSTS, directly translating into wafer fab equipment budget expansions across major foundry and memory customers

AI-driven advanced node demand: Logic and memory advanced node transitions require increasing etch, deposition, and inspection intensity — core capabilities of LRCX, AMAT, and KLAC

Outlook: 4/5 — Strong sector-wide catalyst tied to confirmed memory capex upcycle

Momentum: 3/5 — Recovery underway but decelerating in recent sessions; LRCX and AMAT showing range compression near recent highs

Disclaimer: This content is solely for informational and educational purposes. The content herein does not constitute, and shall not be construed as, financial, legal, or investment advice. It is not an offer, solicitation, or recommendation to engage in any transaction involving securities or other financial instruments.

All insights presented reflect the author’s independent observations and analysis as of the date of publication. This content is not tailored to the specific investment objectives, financial situation, or particular needs of any individual recipient. Accordingly, readers should not make any investment decision based solely on this content without seeking independent professional advice and performing their own due diligence.

Investing in financial markets involves significant risk, including the potential loss of all capital invested. Historical performance data and backtesting results are provided for illustrative purposes only and are not a reliable indicator of future returns. FirstGlow Capital and its affiliates disclaim any liability for losses arising from the use of or reliance on the information contained in this journal.

To read our full disclaimer, click here.